Question: I’m planning to switch from the Income-Based Repayment “IBR” student loan repayment plan to Revised Pay As You Earn – “RePAYE”. How do I accomplish this without having any hangups?

Well – this process varies depending on your circumstances:

Scenario #1

If none of your student loans qualify for RePAYE, the first step is to get them qualified. You can do this by consolidating your non-qualified loans into a new direct consolidation loan. This requires completing the direct consolidation application.

Keep in mind you are NOT required to consolidate all of your loans and instead can pick and choose. Also – consolidation resets the PSLF repayment clock and forces all interest to capitalize.

The most important part of the direct consolidation application is the section where you indicate which loans you’d like to consolidate. If you’re consolidating all your loans, it should be simple. But if not, you should triple check for accuracy before submitting.

Once you’ve completed the consolidation application, you must then complete the income driven recertification “IDR” application. This is where you verify income — which they use to set your new monthly RePAYE payment. Make sure you answer the income related questions accurately and indicate you’d like to enter into RePAYE. After triple checking, submit the form.

This should be all that’s required from you to get the ball rolling. Pay attention to all the correspondence your servicer sends in the months after applying. If you see anything that doesn’t make sense, call them to clarify. Ultimately, it’s not complete until you see the final consolidation loan (in place of all your old underlying loans) and the repayment plan approval for RePAYE.

Scenario #2

Maybe you’d like to move all of your loans from IBR to RePAYE but some of your loans qualify for RePAYE and some don’t. In this situation, you must complete all the steps in scenario #1, except you don’t have to consolidate the RePAYE eligible loans unless you want to. Let’s assume you don’t want to.

For these loans, you should leave them out of the consolidation application and complete a separate IDR application. Indicate that you’d like to change repayment plans from IBR to RePAYE.

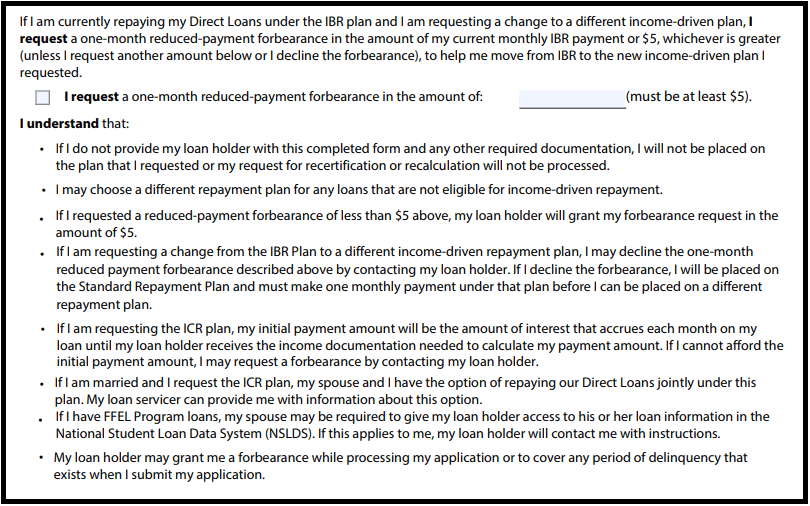

When you are literally changing from IBR to RePAYE, they require a special step. You must either go into a one month reduced forbearance and make a one-time $5 payment or pay one month of the full 10 year standard payment. And this is where the major hangup occurs.

As of this writing, the IDR application has a section that talks specifically about this special requirement. There is even a section where you check a box acknowledging it and write in $5 if you don’t want to pay the 10 year standard payment. If you don’t see it, try looking at the actual pdf that is populated from the online questions.

You would think this straightforward step in the application makes it clear what your intentions are. But it’s not working for the loan servicers.

We’ve learned that for some loan servicers, the IDR application is not enough. And you must literally call them after submitting the IDR application to re-verify this. One servicer called it a “verbal forbearance request”. They read off forbearance disclosures and you must say if you’d like to do one $5 payment or the ten year standard payment. Sounds a lot like the application that you just completed right?

So make sure you call your servicer soon after submitting the paperwork to complete the verbal forbearance request and make the one-time payment. Don’t expect any notification of this requirement either because we’re not sure it exists. And keep an eye on the process. If you notice anything that doesn’t look right, call the servicer.

Scenario #3

If all your loans already qualify for RePAYE, you start by completing the IDR application. Select that you’d like to change repayment plans to RePAYE. Complete and submit the application. And call your servicer several days later to request the one month forbearance and arrange for the one-time payment. Also, keep an eye on all correspondence and call if anything looks off.

Want help navigating this process? Click here to schedule a call and find out more about our student loan advising services.